Part 1: Author’s Bias

All valuations are biased.

I must start with a simple yet profound confession. I love education. And, I love EdTech more. So, why does that matter? Well you see, when going into any analyses, it is important to consider that the analyzer, the person conducting the analysis, may have some preconceived biases. For me, I am more likely than not optimistic on education because I run an EdTech company and love to teach.

The bias starts at the moment you choose a stock. I bet it’s not a random pick. Why did you choose that specific stock? Well, you probably heard of it in passing or tracked it in the past. This means you have a view on it. Given, that view could be positive, neutral, or negative; nonetheless, you have a view. The metrics you choose in the model are affected by that view.

For me, this meant choosing the stock because I like following EdTech and education more broadly. This meant choosing to focus on revenue multiples because most of the peer group operates with negative earnings and trade on lofty growth expectations.

Although, ironically, before researching the name, I became an acerbic critic. Just look at the stock price, will ya. Either management is incompetent or investors got overly bullish on management’s window dressing. Or maybe a mix of both.

Stock down ~88% in the TTM

Stock down ~98% since the last 5 years

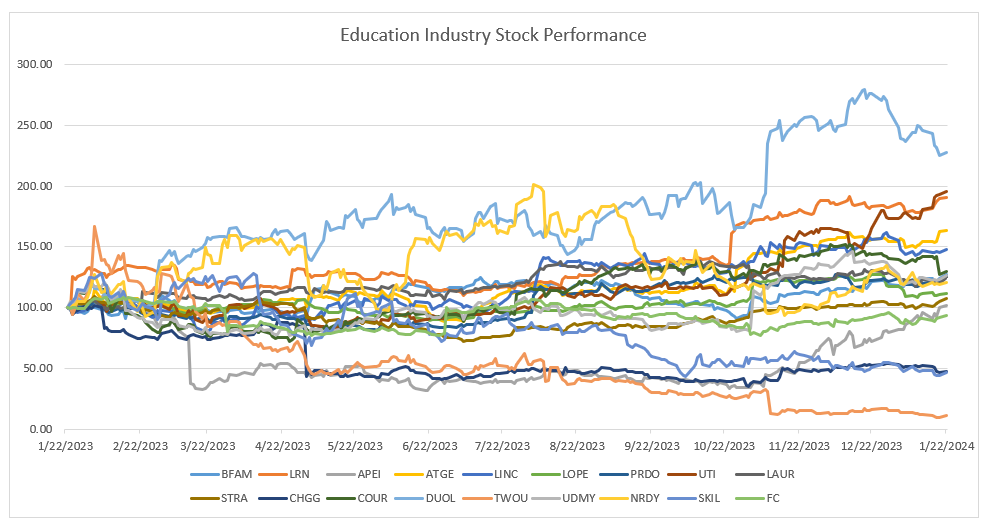

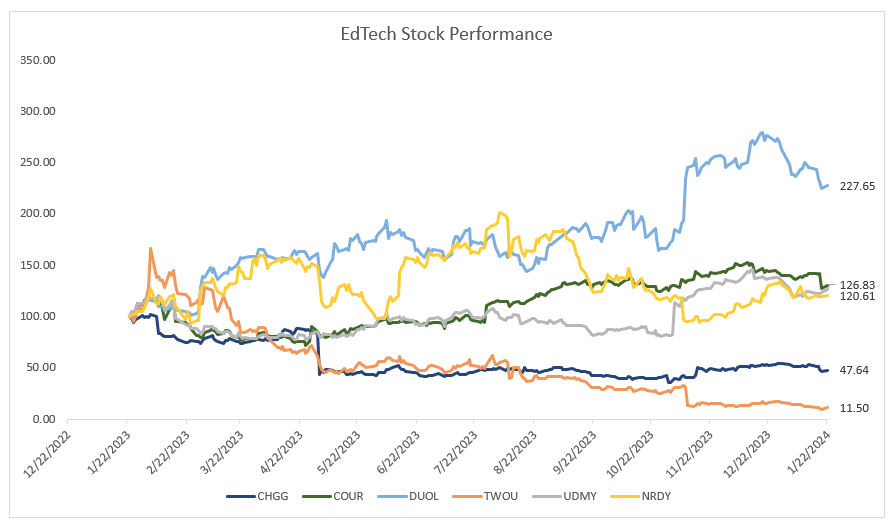

2U has bottomed the education sector. Stripping away most of the postsecondary names to focus on EdTech, it remains the laggard.

Both Chegg (NYSE: CHGG) and 2U (NASDAQ: TWOU) have struggled to keep up with their peers in 2023. Over the past year alone, the market has moved up ~21%. There is commonality between the severe underperformance of both names, an increasingly unattractive core business that is less economically viable.

Chegg – homework solutions migrates to Chat GPT

2U – In-house digital transformation

Additionally, TWOU has tremendous financial difficulties, threatening its existence – more to come. Throughout this write-up, I attempt to be as unbiased as possible by reviewing factual information (financials) as opposed to opinions, but I recognize the following:

Why did I pick the company? Because it grossly underperformed relative to its peers.

Do I like/dislike management? The once revered EdTech pioneer, Chip, has left… Yes.

Do I own the stock? No, I’m as worried as you.

Investors are Biased.

Likewise, we should be wary of comments suggested by large equity investors and equity analysts. They have their own incentives.

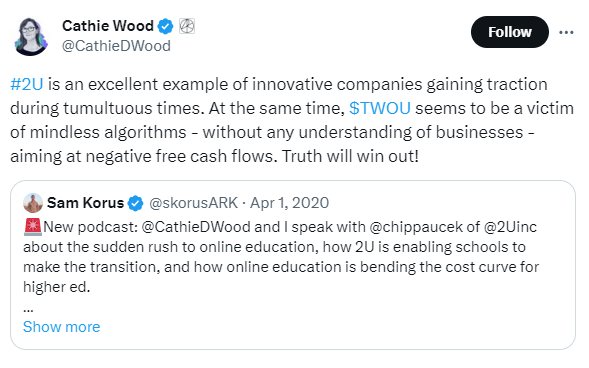

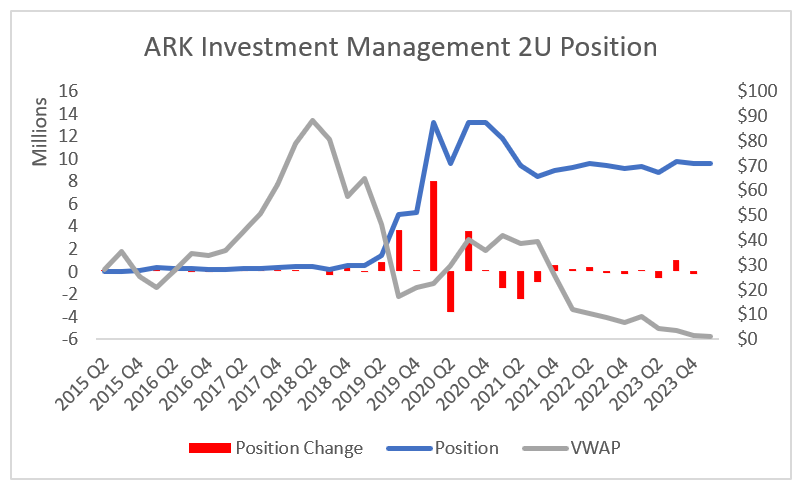

Cathie Wood-led Ark Invest acquired over 1 million shares of the online education platform 2U Inc (NASDAQ:TWOU) in August, 2023.

Cathie Woods has sunk ~$168mm as the company had a multi-billion dollar valuation. Today, the overall company is on the verge of bankruptcy, worth a mere ~$70mm. ARK’s stake that once boasted a ~$531mm valuation in Q3 2020, now sits at a disparaging ~$9mm and change. Talk about value destruction.

Source: Bloomberg, DropoutEdu

Don’t Trust Your Analyst.

In marketing, there was a study that showed, the more (i) precise and (ii) extreme the analyst was in predicting the stock price, the more competent they seemed to the investor. In other words, saying that the stock would move up with a 50% likelihood and move down with a 50% likelihood versus the stock would move up with a 90% likelihood, investors have more confidence in the analyst who is more certain. Although, statistically, we know that the first analyst is likely to be right over any point in time.

“Say wiggle waggle and no one seems interested. Cry fire and everyone runs!” Thornton O’Glove.

Analysts get detailed information from management. Their paychecks rely on maintaining good terms with management teams of stocks they cover. Doing a favor to management by putting out positive to neutral reports will help the bank win future business transactions, including M&A, capital raises, commercial banking, with often hefty fees. So, you will have a predisposition to assuming more aggressive growth rates or lower risk inherent with companies that you seek to maintain relationships with, hint, all of them.

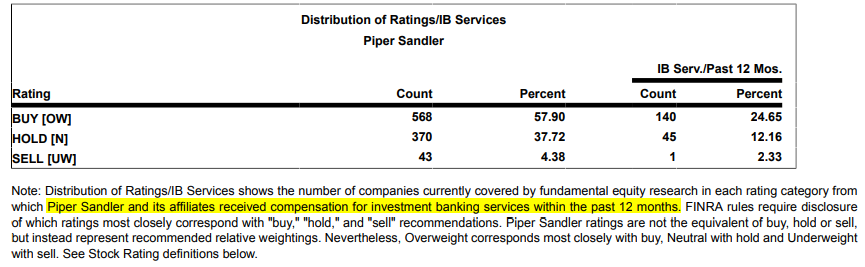

On 2U, there are two updates on Q3 performance by Piper Sandler and Barrington Research.

Further, the investment banks are required to disclose their overall ratings distribution and related investment banking revenues, as shown below.

It is by no coincidence that they do investment banking for a large number of the companies they cover (17% in the LTM). And it is no surprise that only 2% of the firms that got a sell rating with Piper Sandler did investment banking with them. Although there is distortion from the fact that those firms are probably doing worse so will not pursue M&A/other investment banking activities.

Similarly, Barrington research has no companies they cover underperforming. And, they collected investment banking revenue from 27% of the companies rated as outperform.

These disclosures should not be taken with a grain of salt. While research analysts are not compensated “directly or indirectly, related to the specific recommendations or views in this report… research analysts receive compensation that is based on, in part, on overall firm revenues, which include investment banking revenues.”

That is the key line. Your compensation is not directly/indirectly tied to how you rate one specific firm. That is illegal. It would be fraud to put out equity research in favor of a company that is going bust, or even making things appear better than they are in an attempt to have investors part with their money. Fraud. But, when you zoom out, their performance compensation is all about how they can help the investment bank retain such clients to continue generating transaction fees on the back end. Positive research notes is step one in that process.

Wall Street expresses bearishness subtly in the form of various euphemisms:

“Lowering intermediate term rating”

“Stock is not likely to outperform”

“Stock is for patient investors”

It’s all about framing.

Loss aversion: the psychological loss is perceived much greater than an equal psychological gain. So, analysts tend to focus on using positive or neutral language: “intermediate,” “outperform,” or “patient.”

Barrington says that they are …

“reducing our investment rating to market perform”

“the stock is down 62% YTD”

“we continue to be supportive of management’s transition”

“we are moving to the sidelines” – identical to patient investors point

Analysts learn how to frame their opinions to control reactions and maintain relationships early on.

Put out a negative report, lose any inside information that gives your research an edge; lose millions of dollars in future deals; lose trust when speaking with other management teams; maybe lose your job. It is hard for a true Wall Street cynic to exist within a larger bank.

Pro Tip: don’t trust your analyst – they have their own incentives: make money.

Part 2: OPM Industry & 2U Overview

Overview

The Online Program Manager (OPM) industry represents a growing segment of higher education, notably graduate education. OPMs allow universities to significantly extend their reach through online education, attracting international students and establishing a global brand.

Source: HolonIQ

Industry Trends

Market Size & Growth: The global OPM market was valued at over $3 billion in 2019 and is expected to reach approximately $7.7 billion by 2025. This growth is driven by the increasing acceptance of online learning and the expansion of universities offering online degrees (HolonIQ).

Services Offered: OPMs provide marketing, student recruitment, enrollment, tech support, and course design services. Their largest expense is often marketing and advertising; they are experts in recruiting students.

Revenue Models: Traditionally, OPMs have operated on a revenue-sharing model with educational institutions. However, there’s a growing trend towards fee-for-service arrangements as colleges develop their own online learning capabilities in-house.

Strategic Acquisitions & Partnerships: The OPM landscape is marked by active mergers, acquisitions, and partnerships. For example, Academic Partnerships acquired Wiley University Services for $150 million in 2023.

Regulatory Landscape: There’s increasing scrutiny and potential regulatory changes around OPM operations, particularly regarding their recruitment practices and revenue-sharing models. The sector faces challenges around regulatory compliance and ethical practices, especially in terms of recruitment and financial arrangements with educational institutions, more on this later.

Quality and Effectiveness: As the industry grows, there’s a stronger emphasis on student outcomes and the quality of online programs. Debt to earnings, the amount of student loans relative to annual salary of graduates is used by regulators to monitor programs.

2U Overview

Core Business: Digital education platform provider, partnering with over 230 top-tier universities and organizations, offering more than 4,000 online learning opportunities.

Segments:

Degree Program Segment: Focuses on enabling non-profit colleges and universities to offer online degree programs, contributing to approximately 60% of sales.

Undergraduate degree programs

Graduate degree programs

Alternative Credential Segment: Offers premium online courses making up over 40% of sales.

Open courses

Executive education

Boot camps

Micro-credentials

Professional certificates

Growth Strategy: Aims to maintain industry leadership through…

expanding offerings and enrollments with new and existing clients,

evolving portfolio to meet lifelong learning demands,

and growing the enterprise channel and global presence.

Part 3: Differential Disclosure

Differential disclosures arise from differences between the story management shares and what the financials actually indicate. There are many differences between management’s discussion and actual financial reporting (annual report vs 10k). This raises red flags around management’s operations of the business. 2U has been a company on the path to profitability for a while… Management has missed guidance numerous times, and adds a whole lot of window dressing. Some highlights below.

“Our results demonstrate how we’re building a resilient business model that is positioned to drive profitable growth and sustainable cash flows—all while continuing to deliver on our mission.”

Yet, a simple glance at the financials show that the company has continued to dig itself into deeper losses and make overvalued investments in growth to get burnt later down the road.

“Given these trends, 2U has invested over $1.9 billion dollars since inception to help top institutions develop online degree programs.”

The investment itself does not mean anything. We must look at the returns generated on those investments. Clearly, as we will discuss, management has not been good stewards of capital, investing in poor projects that have undergone massive impairments. Take a look at their platform investment, edX, which resulted in trade names being written down by ~$120 million in just the first three quarters of 2023. They have clearly overpaid based on past assessments and also their forward-looking statement to begin to amortize the value of the edX trade name, which was previously classified as an indefinite-lived asset prior to 2023.

“Integral to achieving this level of impact is our revenue sharing model, which aligns the interests of learners, partners, and 2U. Unlike fee-for-service providers that are paid upfront regardless of learner outcomes, 2U only receives our full share of revenue if a learner graduates.”

A clear concern is that this pricing model may not be sustainable. Management has already seen pressures with the 40-60% rev share currently in place; hence, they have switched to a flexible model that allows partners to choose which services they need to maintain costs. The fee-for-service is preferred for universities to keep costs low. Revenue share keeps the university at the mercy of 2U because they need to fill capacity, or else suffer the massive cost of investment.

“We also offered to trade revenue share for affordability to incentivize partners to bring down the cost of higher education. We’ll lower our share of program revenue for partners that meaningfully lower tuition rates. Bringing down the cost of higher education is not only better for the world, it’s better for our business.”

This statement is contradictory. No company would say that negotiating lower rates are a positive to the business. That often means lower revenues. But, the case being made here is that they can have stimulated demand. But, again, that relies on the company to continue to serve demand, which takes it further away from reaching profitability as one of their key goals. Continuing to invest in new programs as we will see is costly. Management has not been able to turn new programs profitable for 2-3 years. Hence, this is misleading. As an investor, I would prefer higher rates with constant maturing demand (aka programs that are already up and running).

Increasing prices overtime has high flow-through margins, meaning that most of the dollar increase in prices will flow-through to increase the bottom-line. Additional volume means additional cost. This is not a sustainable strategy given that it takes 2-3 years to see the profit from those upfront investments. 2U is not in a position to continue to deepen losses for 2 years.

Part 4: Debt Terms

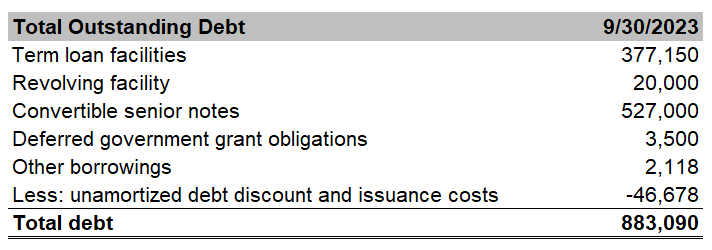

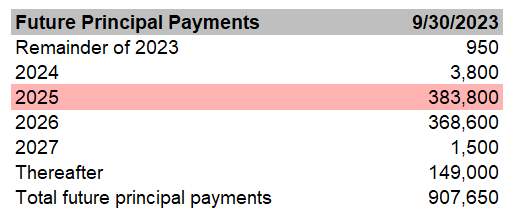

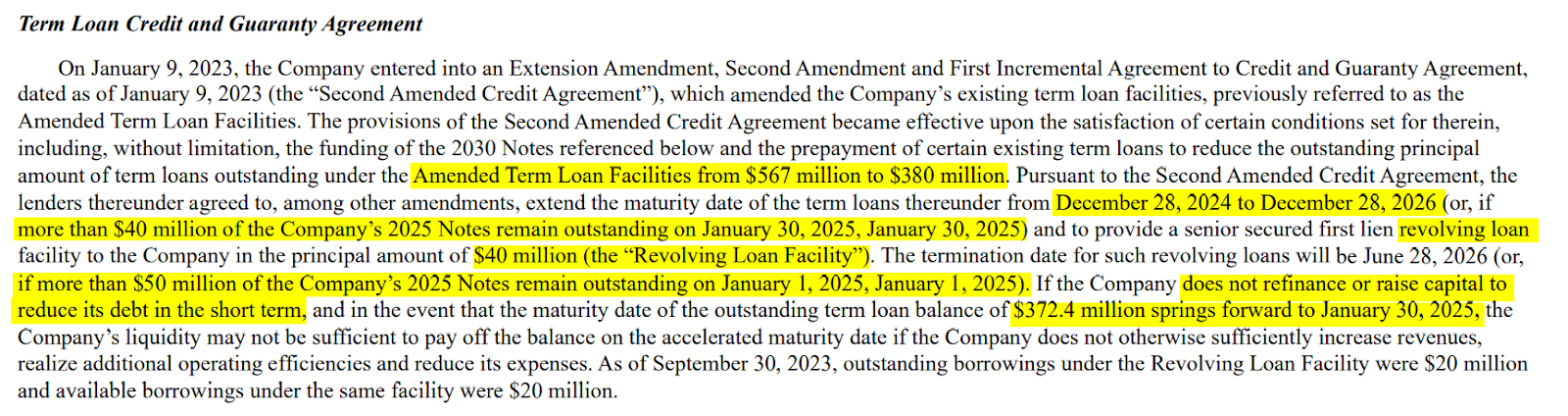

The insurmountable concern for investors is the $380 million in Senior Convertible Notes that matures in 2025.

Source: Company Filings

**Looming Risk**

If the Company does not refinance or raise capital to reduce its debt in the short term, and in the event that the maturity date of the outstanding term loan balance of $372.4 million springs forward to January 30, 2025, the Company’s liquidity may not be sufficient to pay off the balance on the accelerated maturity date.

In short, the company’s acquisitions brought loads of debt to 2U’s balance sheet. Given the company’s high growth prospects throughout COVID with enrollments and revenue soaring, management became overly aggressive. As growth has slowed and profitability was never reached, management is hanging on a thread off a cliff looking for any solutions to right size their balance sheet to restore investor confidence.

Part 5: The Value of Assets

Overview

Let’s break down value into three parts from most to least reliable to isolate growth assumptions.

The Value of Assets

Multiples-based

The Value of Growth

I will start with the most conservative approach which removes any unreliability of information that stems from future expectations focusing strictly on the value of assets on the company’s balance sheet. Then, I will move to determining the value based on valuation multiples. Finally, we must consider the implications of growth. Not because it adds to the value of 2U, but rather quite the opposite. Management’s pursuit of growth at all cost, not exaggerating when I say this, may kill the company.

The Value of the Assets

There are two ways to determine the value of a firm’s assets based on the scenario.

Terminal Decline/Distress: If the firm is not economically viable and cannot turnaround, use a liquidation analysis

Going Concern: If the firm can continue to operate on economically viable terms, then the value of the assets are the cost associated in reproducing those assets, reproduction value, or replacement cost

As described earlier, a simple look at the Company’s balance sheet shows signs of financial distress to the burdensome debt load on the long-term liabilities side. If you believe that the Company is in terminal decline and is economically unviable, which I do because of systematic changes in the OPM market including regulatory risk, in-house transformation, and changing fee structure, then the company should be valued based on what the assets are worth in liquidation.

A quick liquidation analysis will show that all equity investors get wiped out because of the $870mm debt burden, which makes the net asset value negative. Because equity investors have limited liability, they can never be called on to commit additional capital in such instances. So, the max loss for equity is 100%, or, in other words, the entire initial investment.

Adjustments

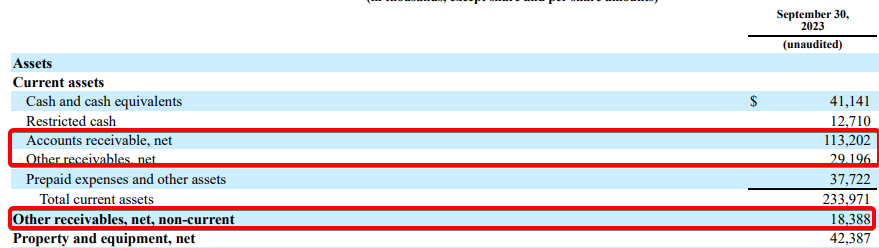

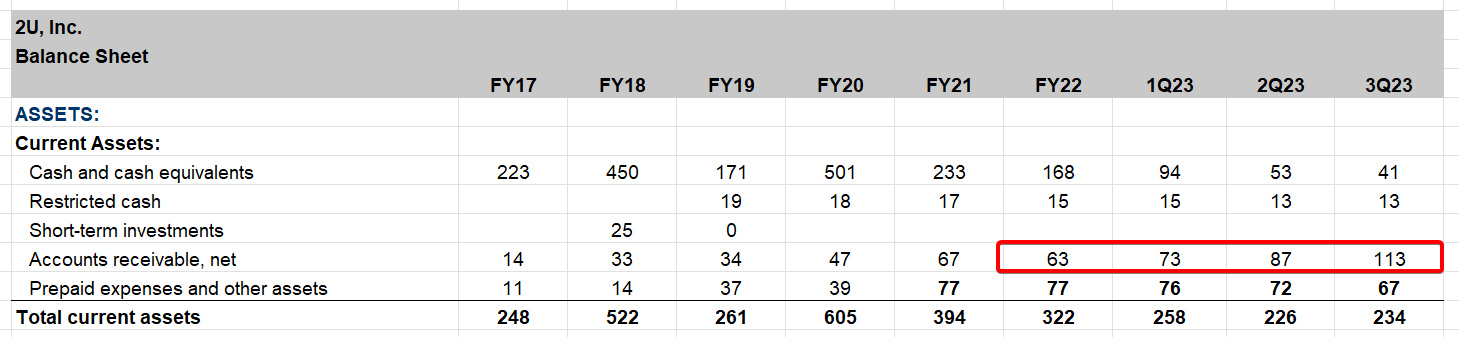

Receivables:

Make adjustments for credit loss and assume that A/R collectors can recover 85% of outstanding A/R. Other receivables, which stem from extended payment plans for the alternative credential segment are already marked at fair value, so we can take management’s word there.

The spike in receivables is temporary and not directly a sign that they are distressed; it comes from closing down programs with existing clients, termination fees. If we assume an orderly liquidation, more on this later, then there will be positive operating cash flows stemming from A/R collection.

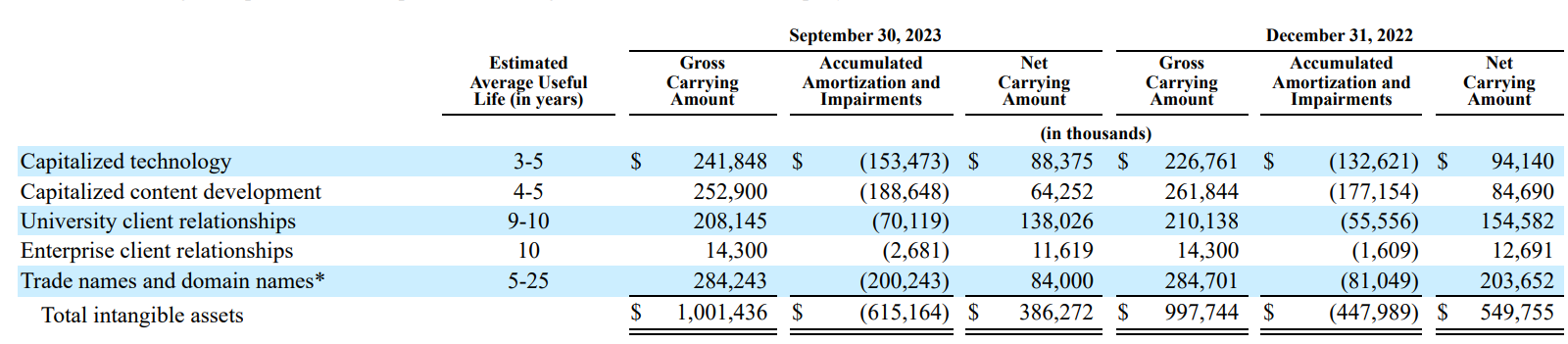

Intangible Assets:

Capitalized Technology has an estimated useful life of 3-5 years which is reasonable, given that infrastructure often grows outdated in half a decade.

Capitalized Content Development has a similar estimated useful life of 4-5 years.

To be on the conservative side when valuing assets, I will assume that it takes 4 years to reproduce the capitalized intangibles. Given ~$27mm in amortization over the past 2 quarters, let’s assume $108mm annualized over 4 years. Then, discount that value based on a fire-sale. It is important to get as accurate as possible on the intangibles because that is the core long-term asset for EdTech companies, which just happens to be less concrete and less reliable.

Source: DropoutEdu

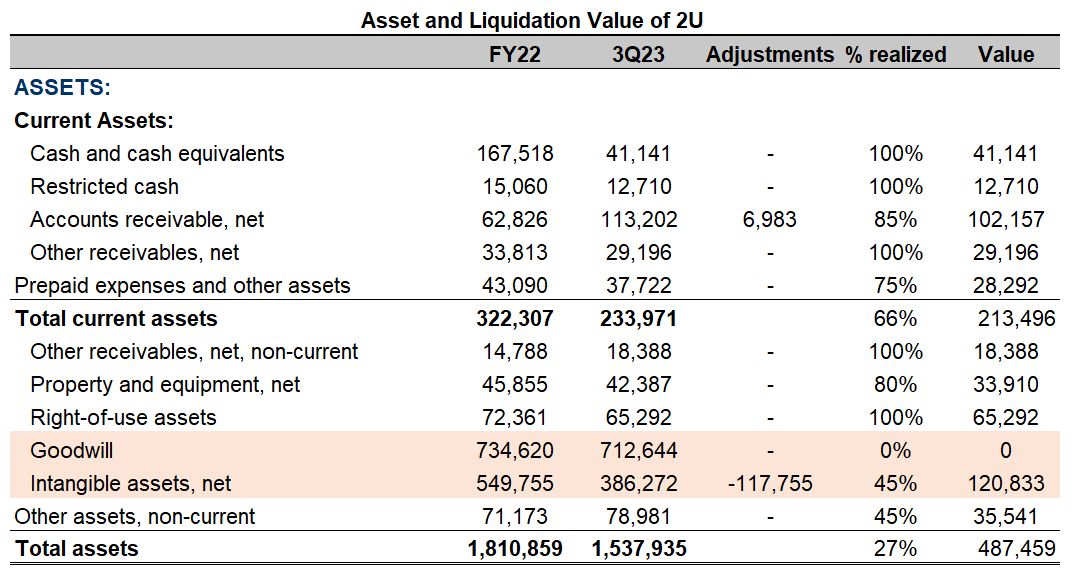

Note that over the past 3 months, just from continuing operations, the company has lost value of assets from ~$658mm to $487mm. The company continuing to operate is destroying value from an asset value approach. This is because the company is burning cash as it attempted to right size its debt earlier in the year.

Assuming that payables, accrued expenses, and other current liabilities net of debt receive priority, there is $173mm left to cover $883mm of debt obligations. In other words, equity investors get wiped out, though distressed debt investors could generate returns depending on where they stand in the capital structure.

Orderly Liquidation

Unattractive, I know. But above is a cynical view that assumes near term liquidation. More common is that firms will undergo an orderly liquidation over the course of 2-3 years. As a result, we can use a NPV calculation because of the short-term projections of cash flow required. The company will be able to generate positive operating cash flow in the near term as A/R comes down, though offset by A/P and DR. However, all of this, again, is dependent on management “staying the course” and winding down operations, overriding the temptation to continue to invest in growth to attempt to extend its life.

At the current stage, management is clearly fighting to clean up its operations and invest in the right direction. On their 3Q’23 earnings call, they mention that the portfolio management activities (switching out of unfavorable degree programs for favorable ones) will generate cash over the next 12-24 months, but they are using this cash to invest in growth. Not ideal.

“From a cash flow standpoint, portfolio management generates near-term cash that strengthens our balance sheet and provides us with the flexibility to launch new programs and invest in our growth areas. Please keep these dynamics in mind as I discuss the results for the quarter and our expectations for the year” Paul Lalljie, CEO

“With unprecedented demand for its ‘flex’ degree model, 2U plans to launch at least 80 new degrees with university partners in 2024” October 2023 Press Release

As a result, it seems unrealistic that management will start to wind down operations anytime soon, especially given the fact that Paul Lalljie just took over as CEO from his original position at CFO with the recent organization change announced in November, 2023. But, we will soon see that this all depends on whether management is able to refinance their upcoming $380mm Term Loan (TL) facility. If they fail to do so, this might mean that an orderly liquidation is the best way to value the company.

Part 6: Choose Your Multiple Wisely

Choosing Comparable Companies

Next, let’s take a look at 2U on a multiples basis. In short, relative valuation is valuing a company based on how similar assets are priced in the market. Those assets should be similar in the following 3 ways:

Free Cash Flows

Risk

Growth

This does not mean that the companies have to be in the same industry although, often, analysts will choose companies in similar industries in order to simplify the selection process of comparable companies. Companies within the same industry are more likely to be similar on the basis of free cash flows generated, risk, and growth. This is more likely the case than not. For instance, take the EdTech industry, companies such as Udemy and Coursera.

These are examples of mid-cap EdTech stocks. Both companies are burning in the range of $55-$75mm of FCF. Both companies have sales in the $500-600mm range and EBITDA of .

Each company is exposed to similar risks based on their business model, collecting subscription payments for access to thousands of courses. They may have similar churn rates, revenue stickiness, etc. They are exposed to the same risks that affect the education industry, which can be more countercyclical because individuals seek education when they are out of the workforce.

Both companies are high growth companies with a historical 1 Yr CAGR of 20-25% and 3 Yr CAGR of 30-40%. Management is focused on growing the top-line to get to profitability with scale. These businesses all have a J curve, make significant investments in infrastructure, university partners, and other to then get a growing return on those investments down the road.

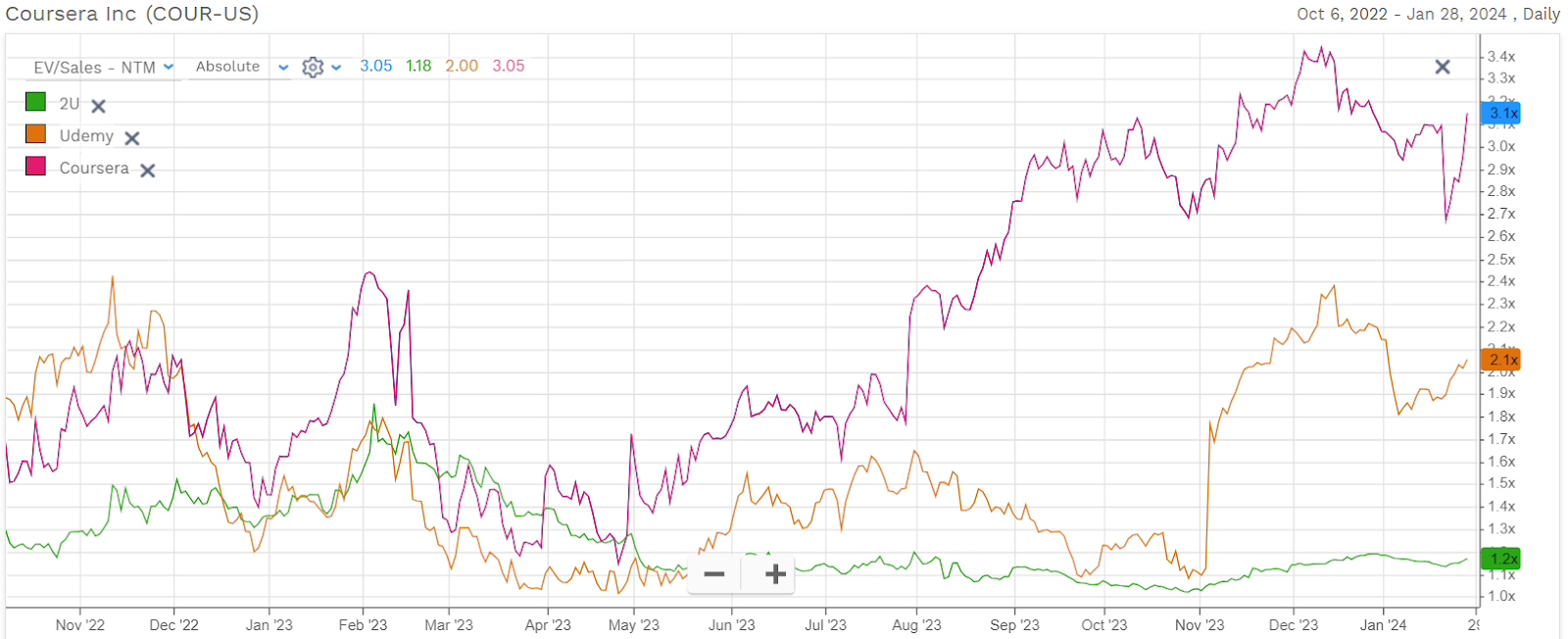

Yet, when you analyze the multiples they trade on, we can see that Coursera trades consistently above Udemy’s multiple. Specifically, Coursera trades at 3.1x NTM sales, whereas Udemy trades at 2.1x NTM sales.

Source: FactSet

The reason? No two companies are the same! No matter how we select the companies in our comparables set, we will still have inconsistencies that arise from different operating structures (some businesses may have higher/low revenue growth, operating leverage, margins, etc) or financing arrangements (higher/lower leverage). Therefore, even businesses within the same industry can be exposed to varying levels of operating and financial risk that are not directly comparable.

The simplest explanation, start at the top-line and think about the pricing model. For instance, Udemy used to sell one-time courses while Coursera implemented a subscription model to provide learners access to all their courses. The difference in pricing model meant that Coursera could increase their customer lifetime value while reducing the amount of costs associated with marketing. Marketing each purchase is a lot harder than simply retaining that same customer. As a result, they can achieve better margins from lower cost and higher expected lifetime value from customers.

Given that both companies offer a subscription model, the real difference? Coursera benefits from the degree programs it offers although it is a smaller part of the overall business. In a rapidly changing landscape affected by generated AI, the value of degree credentials holds value much better than mini courses used for skill acquisition and upskilling.

So the limitation of comps is two fold. (i) There is no guarantee that the multiple properly values the fundamentals of the business (aka its ability to generate cash) and (ii) no two companies are directly alike (it is likely that there are operating and financing differences).

Regardless, in the small set of public EdTech names, this is likely the closest and most precise competitor we can find with reasonable accuracy.

Choosing the Right Multiple

Once you have determined a relevant set of comparable companies based on cash flow, risk, and growth profile, you must select the right multiples to perform the valuation based off. If all companies in your comps set have positive earnings, then we can use most profitability multiples to derive valuation. However, if there are a few companies that are unprofitable in our comps set, then if we were to use a profitability multiple such as price to earnings (P/E), it would return a negative multiple.

Negative multiples do not mean anything. The reason? Imagine you have company A that had -$5 million in earnings and a valuation of $20 million (-4x P/E) and company B that had -$5 million in earnings and a valuation of $30 million (-6x P/E). Clearly, investors are valuing company B higher for the same amount of earnings. But, when you look at the multiples at face value, -6x P/E looks a lot worse than -4x P/E. In short, the multiple flips directionality when it becomes negative. Meaning, companies with negative earnings are more valuable with more negative multiples, and companies with positive earnings are more valuable with more positive multiples. So, we exclude companies with negative multiples because they are meaningless.

BUT, in doing so, we are adding a bias into our comps set. Now our comps set only includes companies that are profitable, assuming that we eliminated all companies with a negative P/E ratio. This will corrupt our data no matter the number of companies you analyze.

Imagine I made a simplifying statement: all unprofitable companies when they turn profitable trade at low multiples of earnings. Then, our statistics from the comps set would be overestimating the true multiple because we excluded the unprofitable comparables. This is a gross simplification that may not be true in practice. But, what is true is that this is not a representative sample, so our statistics from the sample (comps set) are deemed invalid.

Pro Tip: Be skeptical of any multiple artificially constraints the comps set.

Therefore, when I analyze EdTech names, I put a heavier weight on the revenue multiples. The limitation should be obvious. Revenue is very far from cash flows. Just because a company is growing revenues year over year, does not mean it is healthy. In fact, it could go bankrupt the following year. As it’s likely the case with 2U if it cannot manage to refinance its looming debt. Therefore, as investors think about the name based on its forward sales multiple, the price of the asset can quickly diverge from the underlying value of the asset.

Hence, we should be cautious when we use multiples to analyze the sector for the following reasons:

Few publicly traded directly comparable companies in EdTech

Most EdTech companies have negative earnings

Excluding unprofitable companies creates a sampling bias

Revenue is far from free cash flow

Investors get caught up in changes of price rather than levels of price

We will consider Duolingo next week in relation to 2U. A teaser of what’s to come is that Duolingo has lower revenue figures, but are valued at $8 billion by the market. Wow.

Pro Tip: Remember, revenue is not cash flow. Be careful.

Changes to Revenue

Case 1

This is a conservative case that assumes management slows down its growth appetite and cautiously uses that cash that it generates from termination of existing partners under its portfolio management operations to right size its balance sheet.

Assumptions:

Management does not switch into $120 million of revenue because it represents future business from university partners, which is inherently less reliable. Very unlikely since these contracts were signed in 2023

Case 2

Most likely case – management switches into the 80 new university partners to replace the revenue of the partners it has switched out of plus change.

“The Degree business just to highlight the sheer volume of new programs that we’re bringing in. We’ve certainly never seen anything like that. So you’re talking about 80-plus in 2024. You’re talking about $120 million of revenue is at the steady state.” Chip, Co-Founder

Assumptions:

Management successfully conducts their portfolio management activities

Higher discount rate because the firm will continue to suffer losses from additional growth, preventing it from using the cash to right size the balance sheet

Alternative Credits

“Average revenue per FCE decreased 11% and FCE enrollments increased 9%, driven by strong performance of our exec ed offerings, which increased 18% primarily due to continued strength in our Artificial Intelligence courses. Partially offsetting this increase was softness in our largest boot camp vertical, coding. Remember that our exec ed offerings are lower priced than our boot camps. And this shift in mix led to a decrease in average revenue per FCE.”

Enterprise Learning

“Lastly, we continue to see solid growth in our enterprise business, up 22% in the quarter. And based on current performance and a strong enterprise pipeline, believe it is poised to more than double next year.”

“Because the flow-through margins on the enterprise business is higher than the rest of the Alternative Credential segment. So that’s our objective.”

“And as a segment, the Alternative Credential segment, with the growth that we expect to come from our enterprise business next year and the rightsizing of the cost structure”

Pricing Model Transition

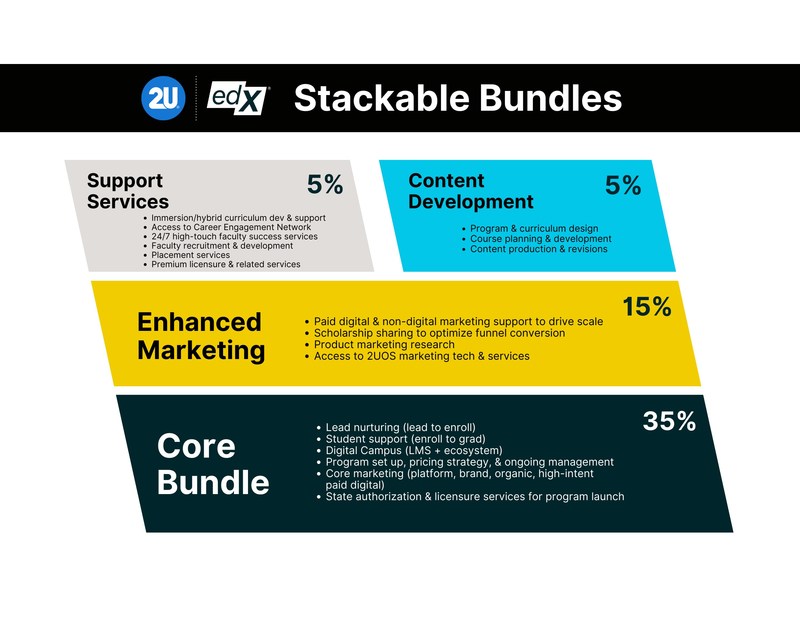

The typical revenue-share agreements in the online program management sector is between 40% and 60%. This means, if the university partner enrolls a student for $40,000, $20,000 is going to 2U over the course of their enrollment.

However, in 2023, management aimed to increase affordability of programs through the revenue-share model because of growing concerns of colleges to support expensive OPM programs that would be costlier than doing it themselves. So they announced the flexible degree model that gives universities the ability to select partnership packages that best fit their needs.

“Our flex model allows universities to obtain our product and service stack with a tiered revenue share model based on what they need. It also allows for a shorter overall contract, which can be desirable for some partners. Most partners have been selecting our core services, plus enhanced marketing and placement for a revenue share of 50% to 55% to 2U. University demand for our flex degrees continues to be incredibly strong. We’re launching over 80 degrees in 2024, up from a previous target of 50, over 70 of which are flex. And we’ve signed contracts for over half of these programs, as you can see in the earnings release. We believe these new degrees can generate $120 million of revenue at steady state and will more than replace the revenue of the degrees being exited through portfolio management.” 3Q2023 Earnings Call

Source: Company Annual Report

“This model lowers our upfront investment and speeds up the timeline to cash flow profitability, while opening the door for more conversations with universities.”

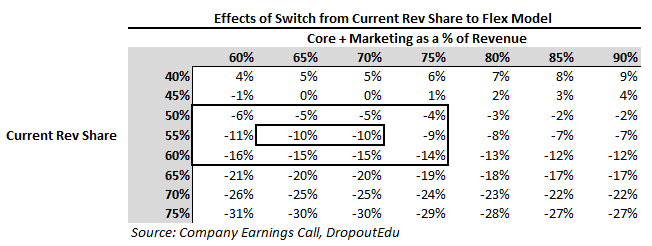

The outcome? Less revenue for 2U with more flexible models. Let’s assume that 2U had an average of 60% revenue share with all of its 230+ partners. If three-fourths of partners opt for the Core Bundle plus Enhanced Marketing, the revenue share is 50%; then for those opting for just the Core Bundle, the revenue share is 35%.

Note that this table assumes 100% transition from the current revenue share model, so the effects will not be as profound in either direction in actual operations because the shift may be more like 90% moving forward. In the 80 contracts in the pipeline for 2024, 70 are flex models.

Also, we should assume a higher Core+Marketing as a percent of revenue because we are not including partners that have >50% revenue sharing contracts. Even if we were to assume that the average was Core + Marketing + one other service (55% rev share), we should still see Revenue fall 5-6%.

Finally, contracts are shorter, meaning lower lifetime value for 2U; so, it is safe to keep the 50% rev share assumption for those on the flex degree.

The outcome, revenue will fall in the range of 5-10%, say 7% on average given the transition in pricing model.

Portfolio Management

Revenue in Q3 2023 into FY2024 is expected to get a boost from portfolio management, closing partner accounts that are low profitability for 2U or do not meet the necessary debt to earnings criteria. 2U had their largest and most lucrative deal early on with USC who in Q3 planned to terminate the contract. Such revenues are from temporary break-up fees and should be accordingly adjusted.

“We had about $7.6 million in the first half of the year. The net revenue impact in 2023 is about $100 million and the cash impact is a little higher because the cash includes – it’s a higher dollar amount than the actual revenue recognized within the period. So the $49 million represents the additional deals that are expected to be signed in the fourth quarter. But the revenue in the fourth quarter already has USC included. So essentially the cash that we expect, the $96 million from the deal’s already signed and the additional $49 million, it adds up to $145 million, which is higher than the revenue that’s recognized.” Paul (CEO) on Q3 Earnings Call

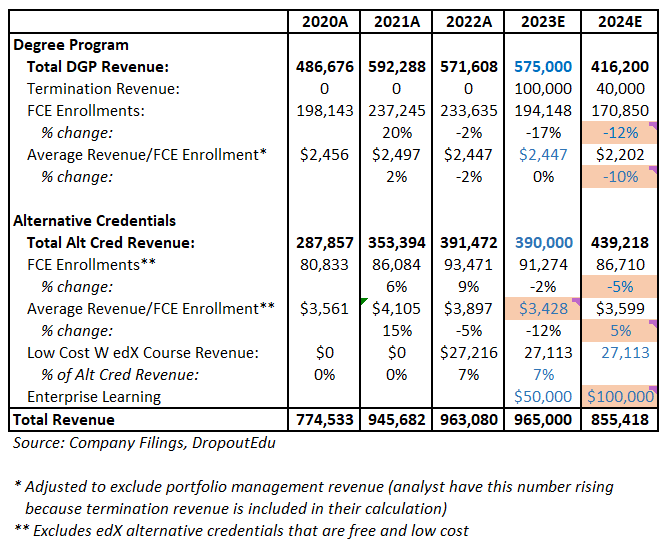

The revenue build below summarizes the net effects given the three changes:

Enterprise: lower average revenue per FCE under the rapidly growing enterprise segment, but higher flow-through margins to offset impacts on profitability

Flex Model: transition from current revenue share to flex model, which allows for lower costs for university partners

Portfolio management: the closing and opening of $100 million and $120 million of revenue

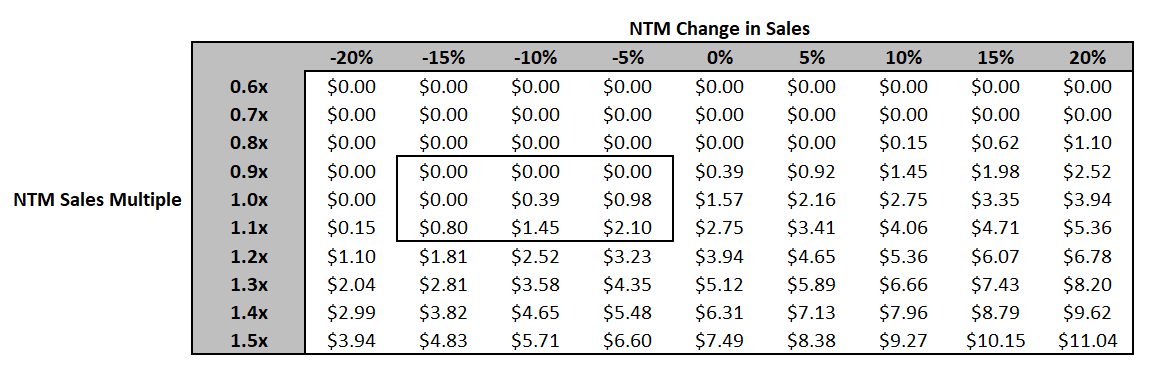

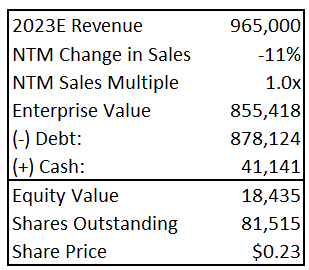

In the table below, I do not use the median multiples of the comparable companies because 2U is distressed and on the verge of bankruptcy. I looked at its historical multiple, which ranged from 1-2x NTM sales and compared this against their NTM sales growth.

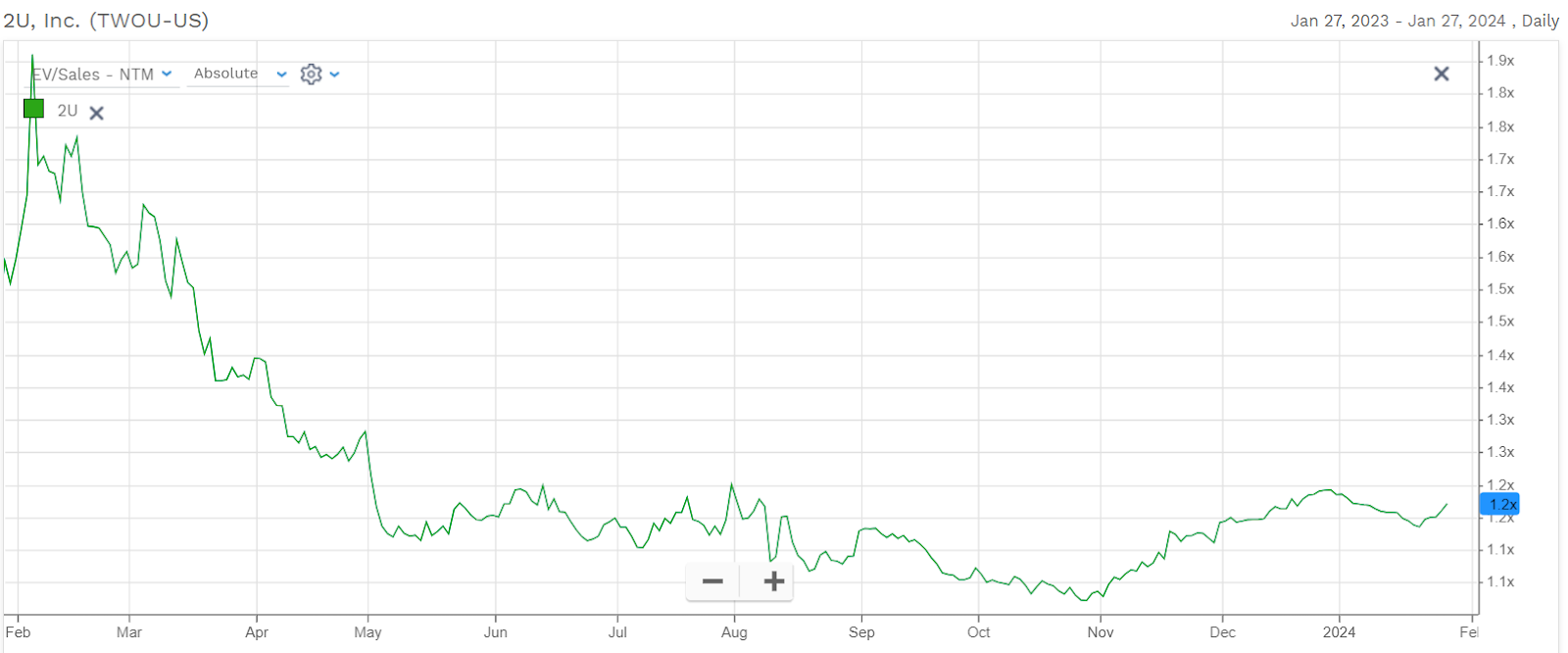

The Company has traded down from a 10x forward multiple at its peak in 2018 to 1.1x NTM Sales, well below its EdTech peer group at 3.4x.

Source: FactSet

For these reasons, I think it is reasonable to see sales decline ~11% YoY into 2024. At a 1-1.1x multiple, this puts the company at $0.39-$1.45. Over the past 30 days, the stock has traded in the range of $0.75-$1.35. This means that from a multiples perspective it is correctly priced. Although, we could see the multiple further compress given refinancing risks.

Source: DropoutEdu

So, we come back to the same conclusion. If the company cannot refinance its looming debt, then the company will probably see its multiple compress even further, making trade for mere pennies. If the company can successfully negotiate extended terms on debt, then it could have more room to run, but the lack of profitability still exists given the interest doesn’t go anywhere nor does the J curve business model disappear.

Takeaway: Just because a stock looks cheap, does not mean it is cheap. There can be serious reasons that the market has pounded it down. In the case of 2U, I think this is justified. I am staying away. But, I will be circling back to it as they report earnings as I think it is an interesting distressed story to watch as the Company has struggled to gain footing and sustain operations after the COVID boom.

Part 7: Growth

Finally, a note on growth. We can assume no value is contributed from growth. Given that the company is trading at distressed levels, if it were to raise debt, it would cost ~13-15%. Yeah, it simply cannot handle that.

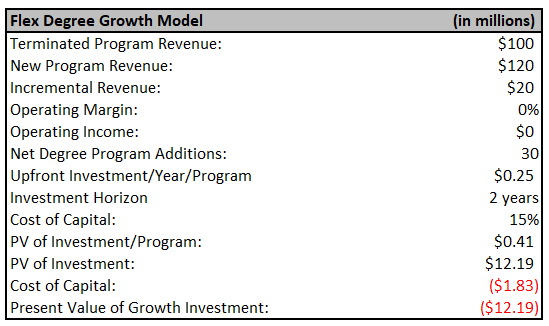

But for the purposes of assessing the effects of growth on value, assume a 15% cost of capital. The company had -$26 million in operating income in 3Q2023. Assuming that the company can realize $55 million from headcount cuts, or $13.5 million in 4Q2023, then the company at a steady state will have an operating loss of $13.5 million. If the company can manage near-term liquidity concerns, then the company will be able to cut back on restructuring costs. Say, it cuts it to $2 million/year. We will assume that the remaining portion will be a part of its recurring business because already distressed companies are likely to face challenges again in the near future. At most, this will bring 2U an operating loss of ~$1.5 million. Given that the new programs already have the existing infrastructure built, we can assume that development costs will fall by $1.5 million. Overall, this means that the investment in growth yields close to 0%.

Any investment in growth where the cost of capital exceeds the internal rate of return (IRR) will reduce the value of earnings by a factor of 6.7x (1/15%). Given that 2U plans to bring on $20 million more in net revenue from new degree programs, even at a lower operating cost due to existing infrastructure and demand established, this will erode the operating value of the firm.

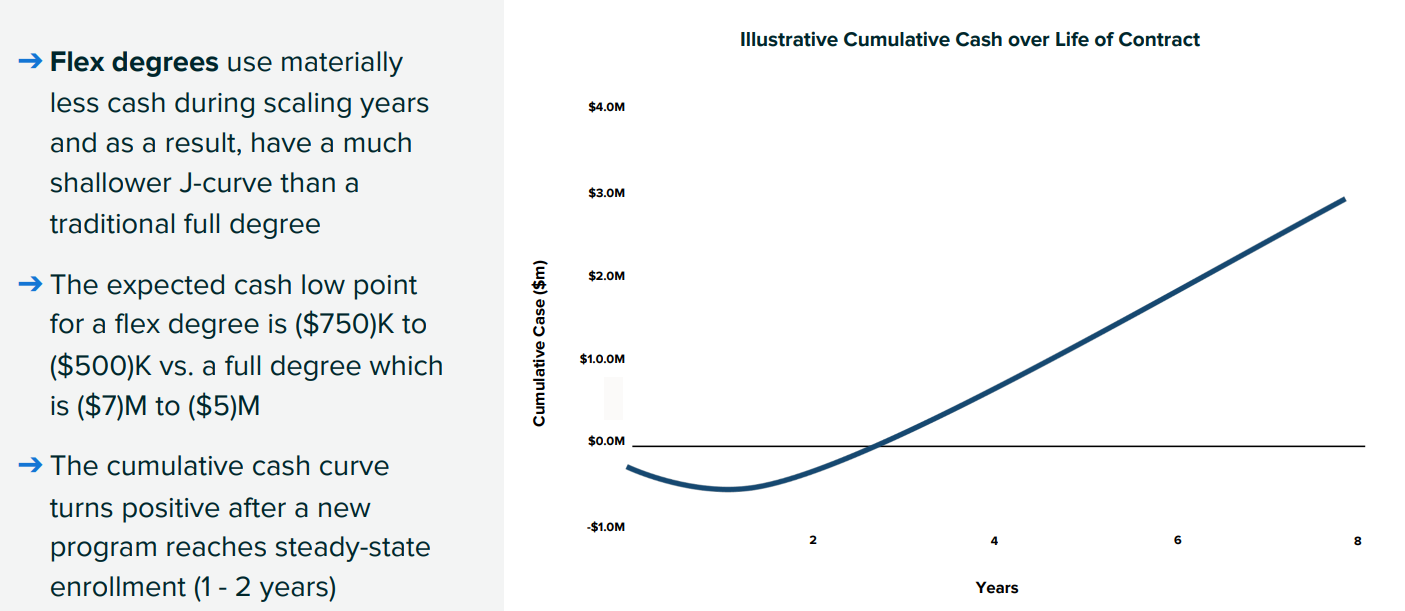

When you look at it from a cash flow perspective, the investment offsets the incremental revenue in the first 2 years. The present value of the initial investment over the first 2 years is ~$12 million. At a 15% cost of capital, the growth destroys ~$12 million in value. Note that this is not a coincidence, it is because the investment is yielding 0%, so you lose the present value of your investment in growth. Sad, but management is unlikely to switch course.

Source: Company Investor Presentation

Source: Company Investor Presentation, DropoutEdu

2U reports earnings on 2/8/2024, and I am focused on the following:

Negotiated terms on the $380 term loan facility.

Cash buffer from portfolio management activities.

Cost savings from headcount reduction and other operational efficiencies without large impact on sales.

But for now, I remain a spectator deep in the sidelines.

Disclosure:

This research report and its contents represent the personal opinions and analyses of the author, intended solely for educational and informational purposes. No representation is made regarding the accuracy, completeness, or timeliness of the information provided, and it should not be construed as professional financial, investment, legal, or tax advice. The financial markets are inherently unpredictable, and past performance is not indicative of future results. The author disclaims any liability for losses or damages arising from the use of this report.

Readers are cautioned that this report is not an offer to buy or sell securities and should consult a professional advisor before making any investment decisions based on the information herein. Accessing this report implies acceptance of these terms, acknowledging that reliance on the report’s content is at the reader’s own risk.